How SMEs Can Use Disclosed Invoice Discounting

Many Indian SMEs sell to large enterprises but still wait 45–90 days for payments. During this wait, payroll, vendor dues, and production costs continue without pause. This puts founders in a tough spot and pushes them to look for short-term funding tied to confirmed invoices.

The challenge often starts with one question: Should you use disclosed invoice discounting or keep it confidential? The answer affects your customer relationship and how collections move. This guide breaks both down in clear, founder-friendly terms.

Quick Summary

- Disclosed invoice discounting informs your buyer; confidential keeps the arrangement private.

- Choose based on your buyer relationships, credit strength, and comfort with collections.

- Lenders assess invoice quality, payment history, and documentation before approval.

- Costs vary by buyer risk, your financial discipline, and the control you want.

- Recur Club guides SMEs on the right structure and connects them with suitable lenders.

Invoice Discounting Basics and What You Must Prepare

Invoice discounting helps SMEs raise funds against approved invoices instead of waiting for long payment cycles from large buyers. It supports raw material purchases, vendor dues, payroll, and new orders that arrive before earlier payments close. To qualify smoothly, founders should prepare:

- Clean records that match POs, delivery proofs, and GST filings

- Reliable buyer payment history with minimal delays or disputes

- Accurate reconciliations showing which invoices are assigned and cleared

- Low-dispute transactions with predictable outcomes

- Recent financial data, like bank statements, GST returns, and ageing reports

For firms with recurring revenue, Recur Club can review revenue patterns and offer funding against stable cash flows, reducing documentation stress.

Disclosed vs. Confidential Invoice Discounting: Key Differences

Recommended: Invoice Discounting: Hidden Costs and How to Manage Them.

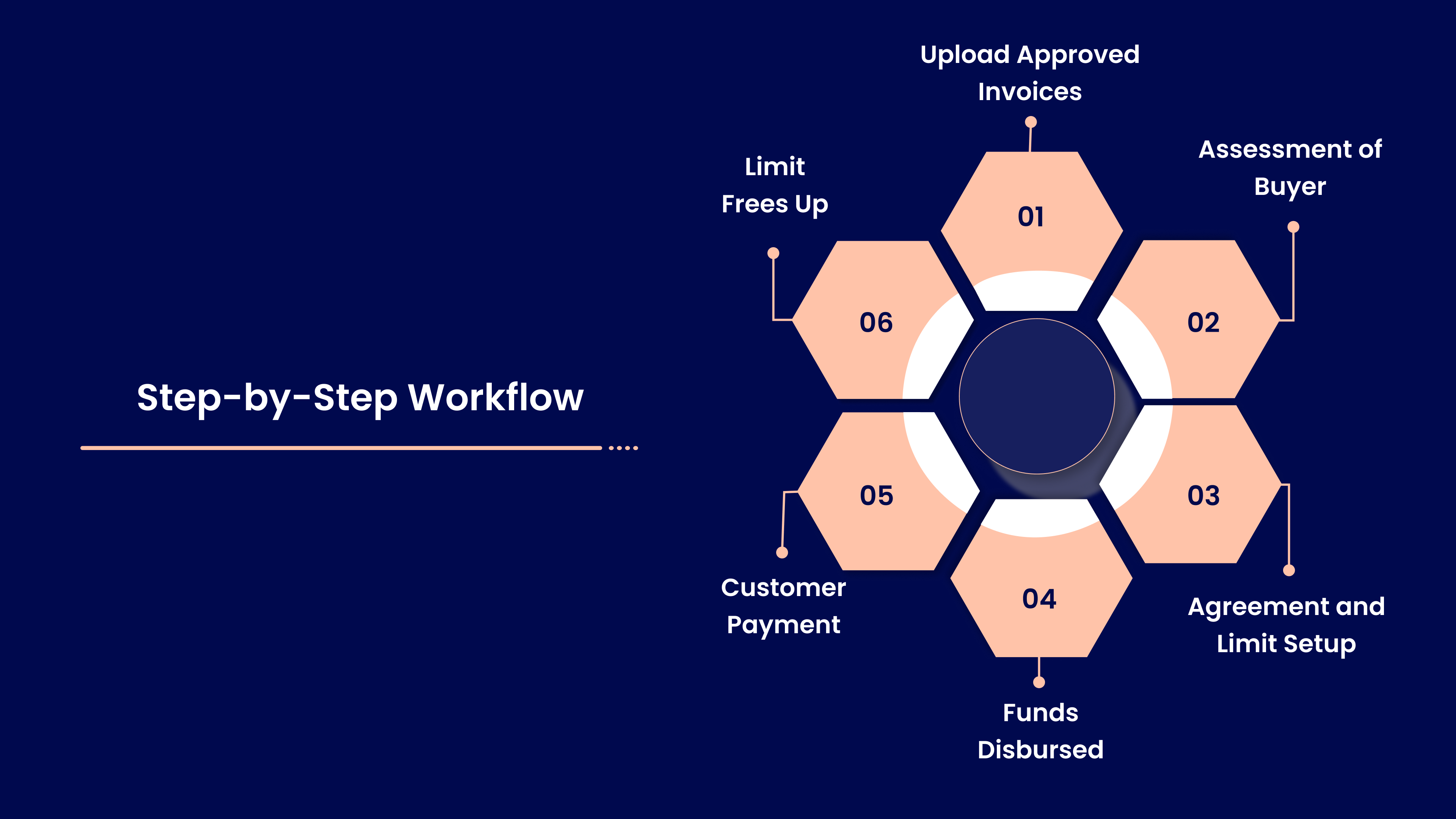

Step-by-Step Workflow: From Invoice to Funding

Here’s a quick view of how invoices move through the funding cycle.

Step 1: Upload Approved Invoices

Share the invoice, purchase order, delivery proof, and GST match. Lenders check if the buyer and invoice meet their criteria.

Step 2: Assessment of Buyer and Invoice Quality

Lenders review the buyer’s payment history, dispute rate, and ageing patterns. This step decides the eligible amount.

Step 3: Agreement and Limit Setup

Once approved, a limit is assigned. Disclosed cases include a notice to the customer; confidential cases skip this step.

Step 4: Funds Disbursed

A percentage of the invoice value is transferred to your account. This helps manage working capital needs while you wait for the buyer to pay.

Step 5: Customer Payment and Settlement

In disclosed models, the customer pays the lender directly. In confidential models, your business collects the payment and settles dues with the lender.

Step 6: Limit Frees Up

Once the settlement is complete, the limit opens again for the next invoice. Platforms like Recur Club offer similar cycles for businesses with recurring revenue or predictable billing.

Recommended: Sources of Working Capital: How SMEs Can Fund Daily Operations.

How Each Model Affects Cost and Control

The cost and control structure differ based on how much involvement the lender has and how predictable your customer’s payments are. These factors also shape how the customer views the arrangement.

Costs

- Disclosed: Usually priced lower because the lender receives payment directly and takes less risk.

- Confidential: May cost more since the lender depends on your team for collections and tracking.

- Platforms like Recur Club: Pricing depends on revenue stability or invoice quality, which can lower costs for businesses with steady billing.

Control

- Disclosed: The lender manages collections, which reduces workload for your finance team.

- Confidential: Your team handles follow-ups, reminders, and reconciliation. This gives you more control but adds internal effort.

Customer Relationship Impact

- Disclosed: Large enterprises are familiar with this model, but smaller buyers may ask for clarity when a notice is issued.

- Confidential: Customer interaction stays unchanged, which works well when you want to keep financing decisions private.

Also Check: Collateral-Free Loans: Meaning and How They Work.

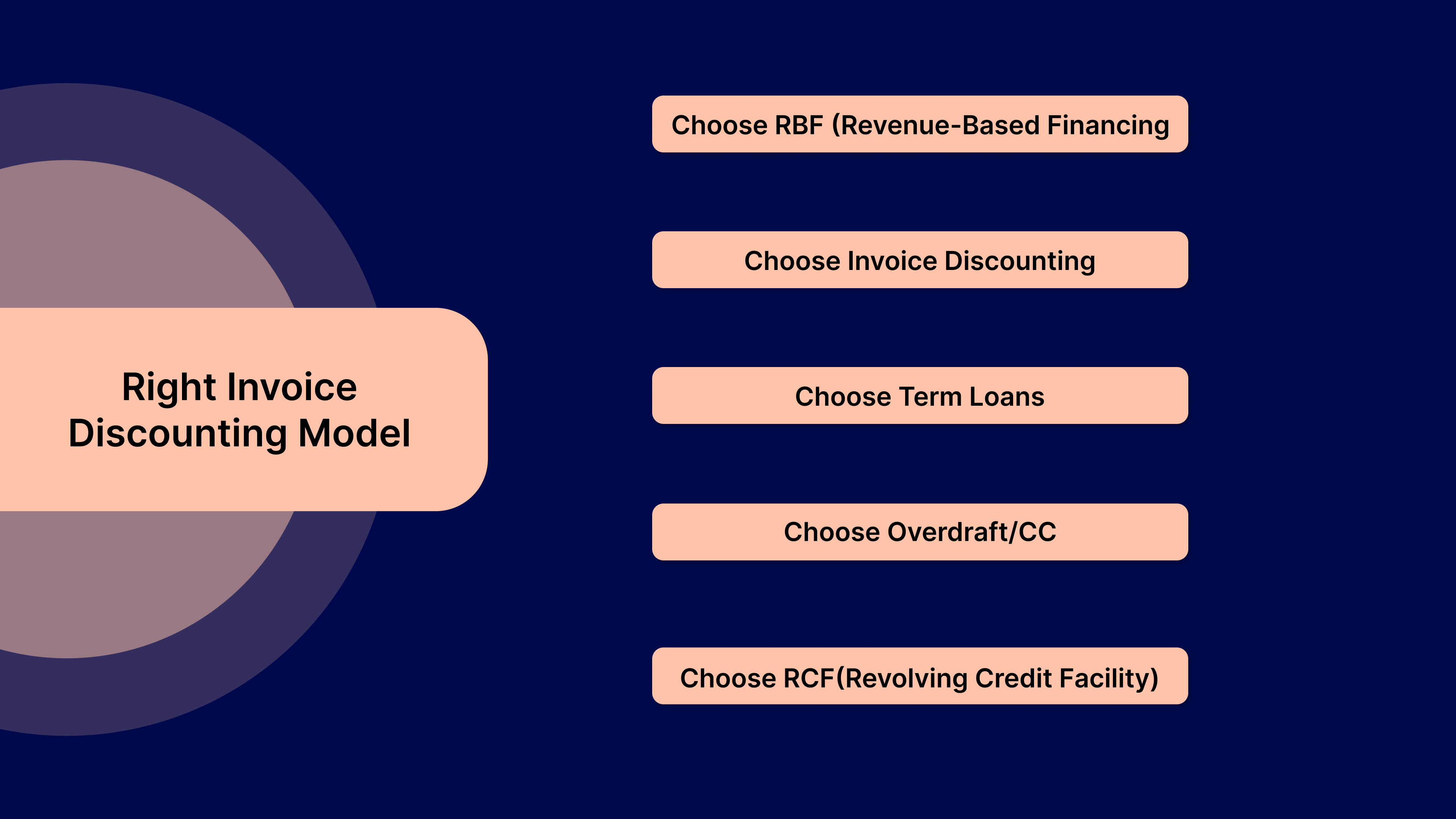

How to Choose the Right Invoice Discounting Model

Use this simple guide to identify the option that fits your current need:

- Choose RBF (Revenue-Based Financing) if you want fast access to funds without collateral and prefer payments that match your monthly revenue.

- Choose Invoice Discounting if you want to turn unpaid invoices into immediate cash while keeping client ownership.

- Choose Term Loans if you prefer fixed EMIs and long-term repayment stability.

- Choose Overdraft/CC if you need recurring access to working capital based on your bank limits.

- Choose RCF(Revolving Credit Facility) if you want a sanctioned limit you can withdraw from as needed, backed by collateral.

Final Thoughts

Disclosed and confidential invoice discounting trade off transparency, cost, and internal effort. Pick disclosed when lender-led collections lower risk, and choose confidential when you need privacy, and your finance team can manage collections. Match the option to your customer profile, internal capacity, and how quickly you need cash.

Recur Club helps Indian SMEs evaluate and execute the right receivables financing option. Key benefits:

- ₹3000 crore+ capital funded; 2000+ customers; 500+ partners

- Expert consultation to decide if debt suits your business and which structure fits best

- Right structure, right lender, right terms tailored to your invoices or recurring revenue

- Frictionless disbursal with hands-on execution until funds reach your account

Ready to convert unpaid invoices into working capital? Book a call with our team to get started today!

FAQ’s

1. Does invoice discounting change GST treatment?

No. GST billing and payment timelines stay the same. You only need to keep invoice, delivery, and return records clear for lender checks.

2. Will this show up as debt on my balance sheet?

Usually, yes, as a short-term liability. Exact treatment depends on your auditor’s policy and the agreement structure.

3. What if the buyer delays or disputes the invoice?

You’re responsible under a recourse facility. Non-recourse shifts risk to the lender but costs more and is less common.

4. Can businesses with many small buyers still use this?

It’s possible, but harder. Lenders prefer invoices from stable, timely-paying buyers. Firms with scattered receivables may get lower limits.

5. How fast does funding normally arrive?

After documents are cleared, funds can arrive within a few days. Timelines vary based on buyer checks and how quickly you share proofs.

.png)